SUBSCRIBE

Enter your Name and Email address to get

the newsletter delivered to your inbox.

Please include name of person that directed you to my online newsletter so I can thank them personally.

Dianne Williams Wildt, MBA

Certified Retirement Counselor®

Since 1983 in the financial services and investment industry

Retirement Pathways, Inc.

4500 Bowling Blvd., Suite 100

Louisville, KY 40207

Phone: 502-797-1258

Email: dianne@retirementpathways.com

Website: www.retirementpathways.com

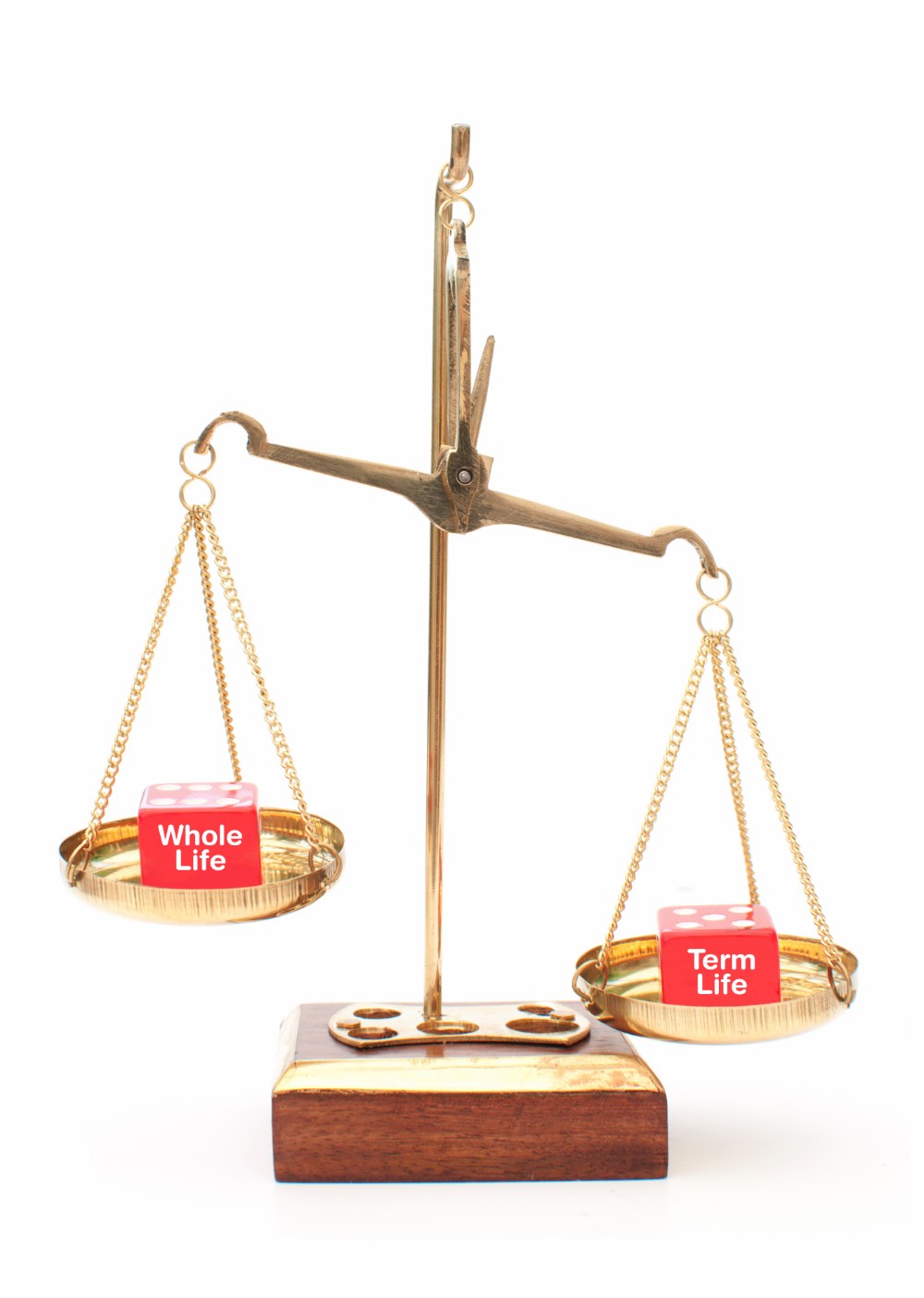

Which type of life insurance is best for you? Term or permanent, the latter shorthand for whole life insurance. Consider the following:

*Applications for life insurance are subject to underwriting. No insurance coverage exists unless a policy is issued and the required premium to put it in force is paid. Life insurance is subject to exclusions, limitations and terms for keeping it in force. Loans and withdrawals from a policy will reduce its cash value and death benefit and increase the chance that the policy may lapse.

Enter your Name and Email address to get

the newsletter delivered to your inbox.

Please include name of person that directed you to my online newsletter so I can thank them personally.

Enter your Name, Email Address and a short message. We'll respond to you as soon as possible.

Investment advisory services offered through American Capital Management, Inc., a State Registered Investment Advisor. Retirement Pathways, Inc. is independent of American Capital Management, Inc.

Retirement Pathways, Inc. and LTM Marketing Specialists LLC are unrelated companies. This publication was prepared for the publication’s provider by LTM Client Marketing, an unrelated third party. Articles are not written or produced by the named representative.

The information and opinions contained in this web site are obtained from sources believed to be reliable, but their accuracy cannot be guaranteed. The publishers assume no responsibility for errors and omissions or for any damages resulting from the use of the published information. This web site is published with the understanding that it does not render legal, accounting, financial, or other professional advice. Whole or partial reproduction of this web site is forbidden without the written permission of the publisher.